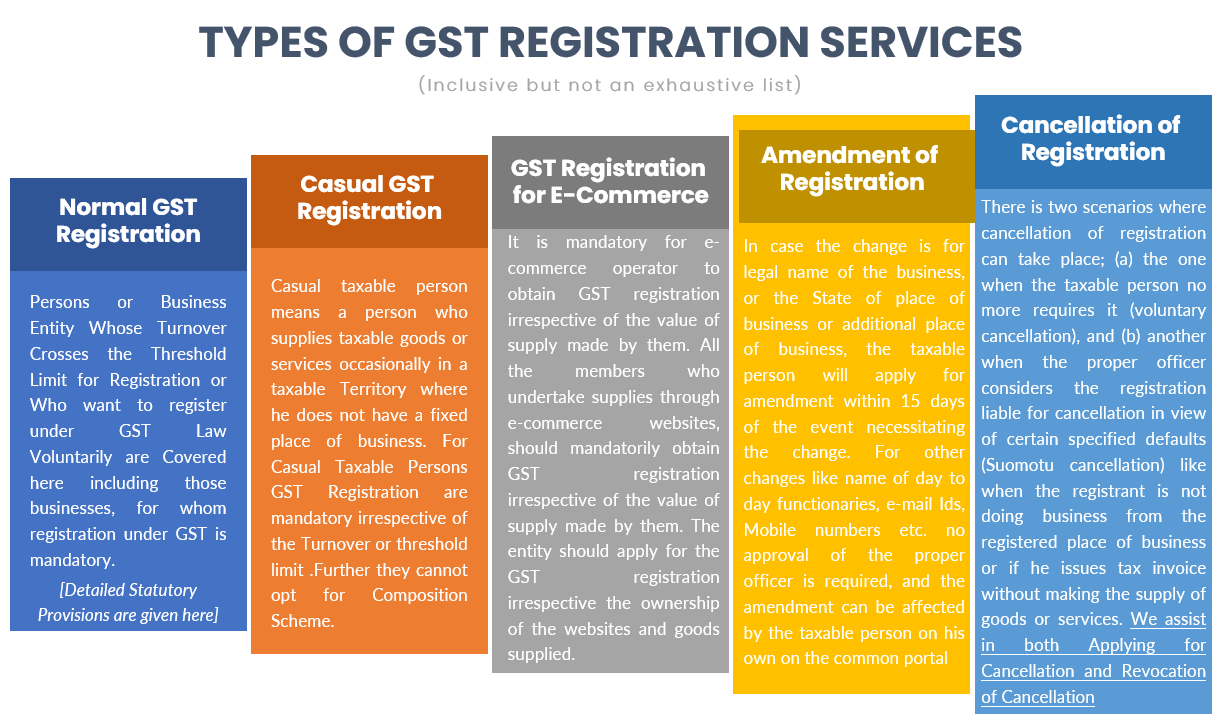

Registration Services Under GST

GST Registration

Goods and Services Tax (GST) is an indirect tax (or consumption tax) used in India on the supply of goods and services.

Registration under the GST Law implies obtaining a unique number from the GST Authorities to collect tax on behalf of the government and to avail Input tax credit for the taxes on his inward supplies. Without registration, a person can neither collect tax from his customers nor claim any input tax credit of tax paid by him.

Need and Advantages of Registration

Registration will confer the following advantages to a taxpayer:

- He is legally recognized as supplier of goods or services

- He is legally authorized to collect tax from his customers and pass on the credit of the taxes paid on the goods or services supplied to the purchasers/ recipients.

- He can claim input tax credit of taxes paid and can utilize the same for payment of taxes due on supply of goods or services.

- Seamless flow of Input Tax Credit from suppliers to recipients at the national level.

Who is Liable to Register?

GST being a tax on the event of "supply", every supplier needs to get registered. However, as per section 22 of Central Goods and Service Tax Act [CGST], small businesses having all India aggregate turnover below Rupees 40 lakh (20 lakhs if business is in Arunachal Pradesh, Himachal Pradesh, Uttarakhand, Manipur, Mizoram, Sikkim, Meghalaya, Nagaland or Tripura) need not register. For suppliers of services, the threshold limit is ₹20 lakh for normal category states and ₹10 lakh for special category states. The small businesses having turnover below the threshold limit can, however, voluntarily opt to register.

As per the changes in the 32nd council meeting, and by virtue of Notification No. 10/2019 – Central Tax, dated the 7th of March, 2019, the threshold limit for GST registration is 40 lakhs for the supplier of goods and 20 lakhs for the supplier of services. Along with that, the North-Eastern States have an option to choose between 20 lakhs and 40 lakhs.

In accordance with sub-section (3) of Section 25, Any person or entity irrespective of business turnover can obtain GST registration at any-time. Hence, GST registration is obtained by many businesses despite not reaching the aggregate turnover limit.

Some of such suppliers who need to register compulsorily irrespective of the size of their turnover are those who are,

In addition, categories prescribed in Section 24 irrespective of the provisions of Section 22 are required to be mandatorily registered such as persons

- Making interstate taxable supply: However, persons making inter-state supplies of taxable services and having an aggregate turnover, to be computed on all India basis, not exceeding an amount of twenty lakh rupees (ten lakh rupees for special category States except J & K) are exempted from obtaining registration vide Notification No. 10/2017-Integrated Tax dated 13.10.2017(AS AMENDED BY NOTIFICATION NO. 3/2019 - INTEGRATED TAX, DATE 29-1-2019)

- Casual taxable persons making taxable supply: A casual taxable person is one who has a registered business in some State in India, but wants to effect supplies from some other State in which he is not having any fixed place of business. Such person needs to register in the State from where he seeks to supply as a casual taxable person. A non-resident taxable person is one who is a foreigner and occasionally wants to effect taxable supplies from any State in India, and for that he needs GST registration. However casual taxable persons making supplies of specified handicraft goods need not take compulsory registration and are entitled to the threshold exemption of Rs. 20 Lakhs. Handicraft goods are specified in Notification no. 33/2017-Central Tax dated 15.09.2017 as amended by Notification No.38/2017-Central Tax dated 13.10.2017.

- Persons required to pay tax under reverse charge,

- Non-resident taxable persons making taxable supply,

- Input service distributor,

- Electronic commerce operator, who provide platform to the suppliers to make supply through it,

- Persons who supply goods through electronic commerce operator who is liable to Tax Collection at source under Section 52. Persons supplying services through e-commerce operators need not take compulsory registration and are entitled to avail the threshold exemption of Rs. 20 Lakhs as per Notification No. 65/2017-Central tax dated 15.11.2017(AS AMENDED BY NOTIFICATION NO. 6/2019 - CENTRAL TAX, DATED 29-1-2019)

- Persons making taxable supply of goods, services or both on behalf of other taxable persons acting as agent or otherwise and the like.

- Those e-commerce operators who are notified as liable for GST payment under Section 9(5) of the CGST Act, 2017

- TDS Deductor

- Those supplying online information and database access or retrieval services from outside India to a non-registered person in India.

Registration for E-commerce seller

Registration is compulsory if you are selling goods online through E-commerce portals maintained by E-commerce operators. The Clause (IX) of section 24 of CGST Act, 2017 provides that persons who supply goods or services or both, other than supplies specified under sub-section (5) of section 9, through such electronic commerce operator who is required to collect tax at source under section 52, has to obtain compulsory registration. Further as per section 10 (2) specifically sets aside the online sellers from this composition scheme.Effective October 1, 2023, composition taxpayers with turnover up to ₹1.5 crore are permitted to make intra-state supplies through e-commerce operators. They cannot pay taxes under composition levy. Unregistered suppliers with aggregate turnover below ₹40 lakh (goods) or ₹20 lakh (services) may make intra-state supplies through e-commerce platforms without mandatory GST registration, subject to conditions.

Composition Scheme under GST

This should be opted at the time of Registration. The Composition scheme under the GST law is for small businesses. This is to bring relief to small businesses so that they need not be burdened with the compliance provisions under the law. Thus, an option has been provided where they can opt to pay a fixed percentage of turnover as fees in lieu of tax and be relieved from the detailed compliance of the provisions of law. Composition levy would be generally opted by persons who are supplying goods & services or both to the end consumer.

At the 32nd GST Council Meeting held on 10th January 2019, and by virtue of Notification No. 14/2019 – Central Tax, dated the 7th of March, 2019, the GST composition scheme limit for states was increased to Rs. 1.5 crore i.e. businesses/individuals with annual turnover of up to Rs. 1.5 crore can opt for registration under the GST composition scheme (applicable from 1st April 2019 onwards). A lower limit for the GST composition scheme turnover limit will be applicable to the North Eastern States and hill states such as Sikkim or Himachal Pradesh which is ₹75 lakh.

Further Composition Scheme is extended to suppliers of Services and Mixed Suppliers (Notification No. 02/2019 – Central Tax (Rate), dated the 7th of March, 2019): Composition Scheme is now made available for Suppliers of Services or Mixed Suppliers (having an Annual Turnover in preceding Financial Year upto Rs 50 lakhs) with a tax rate of 6% (3% CGST + 3% SGST)